Short answer: Yes, impact sliding glass doors can lower your Florida home insurance, but not by themselves and not as a flat dollar amount. Florida law (Fla. Stat. § 627.0629) requires insurers to give premium discounts for storm-hardening features, and impact-rated glazing counts toward the “opening protection” credit on the state’s wind mitigation inspection form. The catch: that credit usually applies only when all of your home’s windows and doors are protected, and the exact savings depend on your insurer, your home, and your inspection results. Confirm specifics with your own carrier before you buy.

We’re JDM Sliding Doors, a family-owned sliding door and impact window company based in Fort Lauderdale (Florida license CGC1536404), and we install impact glass across Broward, Miami-Dade, and Palm Beach every week. This post stays narrow on one question homeowners keep asking: how impact sliding glass doors actually move the needle on your insurance through wind mitigation. If you want the broader case for upgrading, see our reasons to switch to impact windows in South Florida and our breakdown of impact glass doors vs. hurricane shutters. For the storm side of things, our guide to sliding door hurricane protection covers what to do before a storm. Here, we’ll talk dollars and inspections.

Key Takeaways

- Florida law (§ 627.0629) requires insurers to offer discounts for wind mitigation features, including impact-rated opening protection.

- Impact sliding glass doors qualify as “opening protection,” one of the most valuable credits on the OIR-B1-1802 wind mitigation inspection form.

- The opening protection credit generally requires every glazed opening (windows, doors, skylights) to be protected, not just one slider.

- Savings vary widely by insurer, home, and roof features; there is no fixed dollar figure, so get a quote from your own carrier.

- In Miami-Dade and Broward, the door must carry a Miami-Dade Notice of Acceptance (NOA) and be installed under a permit to count.

- A wind mitigation inspection is valid for up to five years, so the paperwork keeps earning the discount long after install.

Do Impact Sliding Glass Doors Lower My Insurance?

They can, through a specific mechanism: wind mitigation credits. Florida homeowners’ insurance is priced partly on how likely your house is to be damaged in a hurricane. When you harden the building so it’s less likely to fail, the insurer’s expected loss drops, and state law passes part of that saving back to you as a premium discount.

Impact-rated sliding glass doors help on the part of your home most likely to fail in a storm: the openings. If a flying branch breaks a slider during a hurricane, wind pressurizes the inside of the house and can lift the roof or blow out walls. Laminated impact glass keeps that opening sealed even when the glass cracks, which is exactly the risk reduction insurers reward. So the discount isn’t for the door itself, it’s for what the door does to your home’s overall storm resistance.

One honest point up front: replacing a single sliding glass door rarely earns the full credit on its own. The opening protection credit is usually all-or-nothing across the whole home. More on that below.

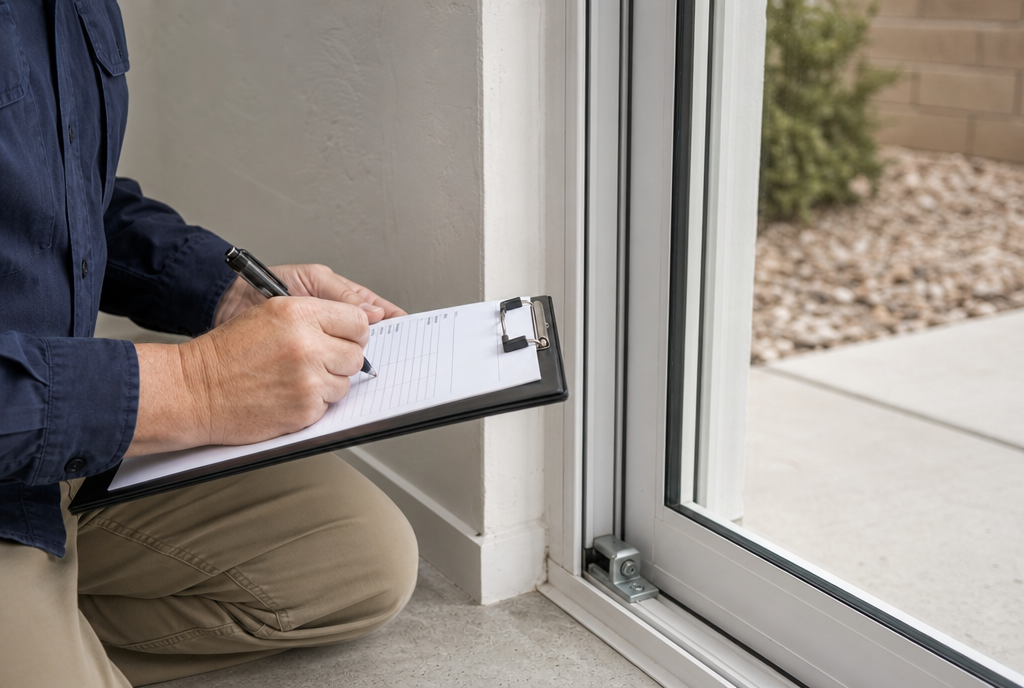

What Is a Wind Mitigation Inspection?

A wind mitigation inspection is a short, standardized assessment of how well your home resists hurricane wind, performed by a licensed inspector, contractor, engineer, or architect. The results go on Florida’s Uniform Mitigation Verification Inspection Form, OIR-B1-1802, which every Florida insurer accepts. You hand that form to your carrier, and they apply whatever credits your home qualifies for.

The inspection checks seven main features:

| Feature inspected | What it looks at |

|---|---|

| Roof covering | Whether the roof meets current Florida Building Code |

| Roof deck attachment | Nail size and spacing holding the deck down |

| Roof-to-wall connection | Clips, straps, or wraps tying roof to walls |

| Roof geometry | Hip roofs resist wind better than gable |

| Secondary water resistance | Sealed roof deck under the shingles |

| Opening protection | Whether windows, doors, and skylights are impact-rated or shuttered |

| Building code / year built | When the home was built or last re-roofed |

Opening protection is the line that impact sliding glass doors affect. The inspection is valid for up to five years, so one inspection can keep delivering the discount across multiple renewals. Source: Florida Office of Insurance Regulation, OIR-B1-1802 (current form).

How Impact-Rated Glazing Factors Into the Opening Protection Credit

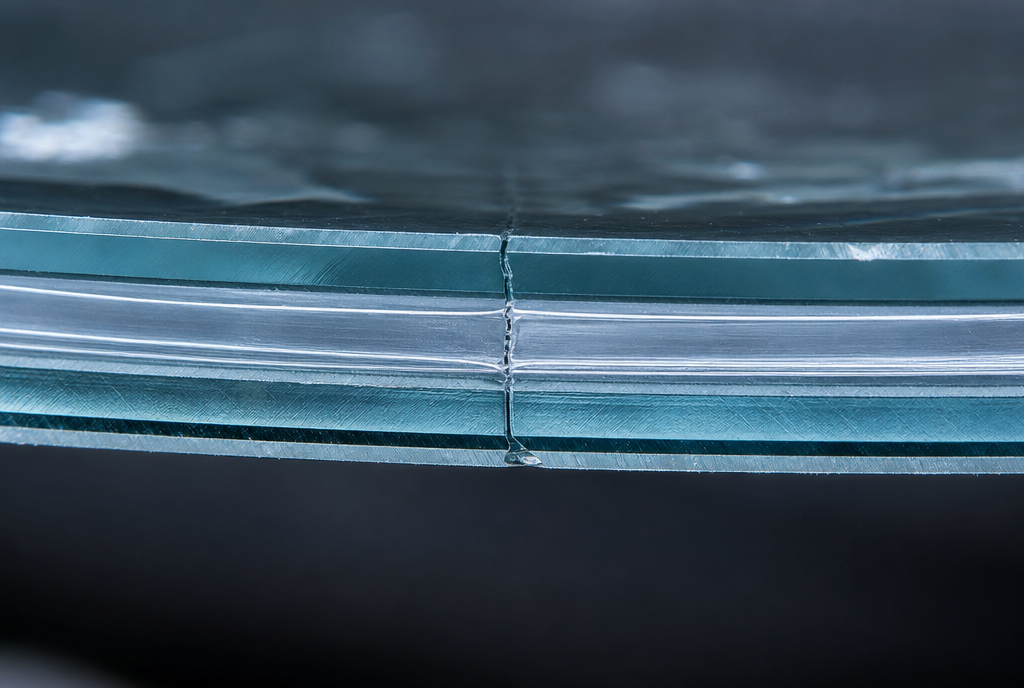

Here’s the mechanism in plain terms. On the OIR-B1-1802, the inspector classifies your opening protection into a level based on how well your openings are covered. To earn the strongest opening protection credit, all glazed openings (and often the non-glazed ones too, like entry and garage doors) have to be protected by a product rated for large-missile impact.

“Large-missile rated” means the product passed a test where a lab fires a roughly nine-pound piece of lumber at it at high speed, then cycles it through thousands of pressure swings. Impact sliding glass doors with a Miami-Dade Notice of Acceptance (NOA) meet that standard. An NOA is a Miami-Dade County document proving the exact product passed those tests.

What this means for your project:

- Protect every opening to get the full credit. If you put impact glass on the patio slider but leave bare windows elsewhere, the inspector generally can’t give the top opening protection level. Many homeowners phase the work, but the biggest insurance jump comes when the last opening is covered.

- Mixing is allowed. Impact glass on the doors and code-approved shutters on the windows can together satisfy opening protection. We compare those approaches in impact glass doors vs. hurricane shutters and impact windows vs. shutters as a long-term investment.

- The product and the install both have to qualify. An NOA door installed without the right anchors won’t pass. In Miami-Dade and Broward (Florida’s High-Velocity Hurricane Zone), the work must be permitted and inspected.

How Much Can I Save?

This is the question everyone asks, and the honest answer is: it depends, and we won’t quote you a number we can’t stand behind. Opening protection is widely considered one of the more valuable wind mitigation credits because openings are a home’s weak point, but the actual discount varies by insurer, your home’s other features (roof especially), your location, and your policy.

A few things shape the size of the credit:

- Your roof. Opening protection often stacks with roof credits. A home with a hip roof, good roof-to-wall straps, and full opening protection sees more total discount than one earning opening protection alone.

- Your insurer. Each carrier files its own discount schedule with the state, so two homes with identical inspections can see different dollar amounts from different companies.

- Your starting premium. A percentage credit is worth more on a high South Florida premium than a low one.

The right move: ask your insurance agent for a quote that shows your premium with and without full opening protection, then weigh that annual saving against the install cost. For the cost side, our guide to hurricane impact window and door cost lays out the ranges. Treat the insurance discount as ongoing savings that compounds over the years you own the home, on top of the storm protection and the lower energy bills.

Fort Lauderdale Impact Sliding Door Installation Done Right

For the credit to actually land, the paperwork has to be clean. That’s where a licensed local installer matters. When we handle a Fort Lauderdale impact sliding door installation, or a full sliding glass door replacement, we pull the permit, install to the NOA, and leave you with the documents your inspector and insurer will ask for: the NOA, the permit, and the final inspection sign-off. Keep those in one folder. Five years from now, at renewal, they’re what keeps the discount in place.

If your current slider is older, leaking, or off its track, replacing it with impact glass solves the storm risk, the insurance angle, and the daily annoyance at once. And if you’re across Broward, Miami-Dade, or Palm Beach, we serve all of South Florida.

Frequently Asked Questions

Do impact sliding glass doors lower my home insurance in Florida?

They can, and the mechanism we explain to Florida homeowners every week is wind mitigation credits. Florida law (Fla. Stat. § 627.0629) requires insurers to discount premiums for storm-hardening features, and impact-rated doors count toward the opening protection credit on the OIR-B1-1802 inspection form. In my experience the catch surprises people: that credit usually requires all of your home’s openings to be protected, and the exact amount depends on your insurer and home, so confirm with your own carrier before you count on a number.

What is a wind mitigation inspection in Florida?

It’s a standardized assessment of how well your home resists hurricane wind, recorded on Florida’s Uniform Mitigation Verification Inspection Form (OIR-B1-1802). A licensed inspector checks the roof and opening features, then you hand the form to your insurer to apply whatever credits you qualify for. One detail we remind clients of: the inspection stays valid for up to five years, so the paperwork keeps earning the discount across renewals.

How much will I save on insurance with impact doors?

There’s no fixed amount, and I won’t quote you a figure we can’t stand behind. Opening protection is widely considered one of the more valuable wind mitigation credits because openings are a home’s weak point, but in practice the savings swing with your insurer, your roof and other features, your location, and your starting premium. The move we recommend: ask your agent for a quote showing your premium with and without full opening protection, then weigh that annual saving against the install cost.

Do I have to upgrade every window and door to get the discount?

Usually yes, if you want the full opening protection credit, because in my experience it’s generally all-or-nothing across the whole home. We see plenty of homeowners phase the work, and that’s fine, but the biggest insurance jump comes when the last opening is finally covered. You can mix impact glass on the doors with code-approved shutters on the windows, just know that one protected slider while the rest sit bare typically won’t earn the top credit.

Does the impact door need a permit and a Notice of Acceptance?

In Miami-Dade and Broward (Florida’s High-Velocity Hurricane Zone), yes, and this is where we see DIY and uninsured installers cost homeowners the credit. The door has to carry a current Miami-Dade Notice of Acceptance, and the installation must be permitted and inspected, because both the product and the install have to qualify. When our crew finishes a job we leave you the NOA, the permit, and the final sign-off, since that’s exactly the paperwork your inspector and insurer will ask for.

Sources

- Florida Statutes § 627.0629, “Residential property insurance; rate filings” (premium discounts for wind mitigation). Florida Legislature.

- Florida Office of Insurance Regulation, Uniform Mitigation Verification Inspection Form, OIR-B1-1802 (current edition).

- Florida Building Code, High-Velocity Hurricane Zone provisions; Miami-Dade County Notice of Acceptance (NOA) product approval program.

Ready to find out what impact sliding glass doors could do for your premium and your peace of mind? Get a Free Estimate and we’ll assess your doors, your home’s openings, and the paperwork you’ll need for the insurance credit.